Disclaimer:

I’m a tech and personal finance enthusiast, not a certified financial planner. This guide is for educational purposes. Always consult a qualified professional for personalized financial, tax, or legal advice before making big money moves.

Let me guess: you’ve tried budgeting before. You opened a blank spreadsheet, enthusiastically typed in categories like “Groceries” and “Fun Money,” tracked every penny for exactly nine days, and then completely abandoned it after an unexpected $400 car repair ruined your perfectly planned math.

I know exactly how that feels because I did it for years. The traditional advice of “just stop buying lattes” or tracking every single cent manually is a guaranteed recipe for burnout. We aren’t robots. A real, functional budget needs to account for variable income, sudden emergencies, and the fact that sometimes, you just really want to order takeout without feeling guilty.

In this guide, I’m going to walk you through how to actually build a monthly budget that works. We’ll look at the best frameworks, the modern tech stack that automates the boring stuff, and specific hacks for freelancers and couples.

The “YMYL” Rule for Finance Sites

If you’re reading this as a fellow creator or blogger looking to monetize your site, you need to understand how Google views money content. Finance falls strictly under “Your Money or Your Life” (YMYL).

Because bad financial advice can ruin lives, search engines demand extremely high E-E-A-T (Experience, Expertise, Authoritativeness, and Trustworthiness). If you want Google AdSense approval, you can’t just recycle generic textbook advice. You need clear author bios, verifiable facts, secure site protocols, and robust disclaimers. Treating your content with this level of professional respect is the only way to build trust with both your readers and advertising platforms.

Establishing Your Baseline

Before picking an app or a framework, you have to know what it actually costs to keep your life running. Generic budgeting templates fail because they ignore reality. You might tell yourself you’ll only spend $300 a month on food, but the average American spends roughly $370 to $500 per person on groceries every single month depending on the state.

Here is how you find your baseline:

Look at your last three months of bank statements.

Tally up your non-negotiable fixed costs: Rent/mortgage, utilities, insurance, childcare, and minimum debt payments.

Find your average variable necessities: Groceries and gas.

Once you know your absolute survival number, you can pick a framework that actually fits your income.

Finding Your Budgeting Framework

There is no “best” way to budget. The right method is the one you will actually stick with. Let’s break down the four most effective frameworks I’ve tested.

1. Zero-Based Budgeting (ZBB)

With ZBB, every single dollar gets a job the moment it hits your bank account. If you make $4,000 this month, you assign exactly $4,000 to your categories (including savings and investments) until your “Left to Budget” number hits zero.

The Good: It gives you total control and is incredibly effective for aggressively paying off debt.

The Bad: It requires high maintenance. If you fall behind on categorizing transactions, catching up feels like a chore.

2. The 50/30/20 Rule

This is the classic, low-stress method. You split your after-tax income into three buckets :

50% Needs: Housing, basic food, minimum debt, utilities.

30% Wants: Dining out, vacations, hobbies, streaming services.

20% Savings/Debt: Investments, emergency funds, extra debt payments.

The Verdict: Great for beginners, but in high-cost-of-living areas, keeping needs under 50% can be mathematically impossible.

3. The Conscious Spending Plan

Popularized by Ramit Sethi, this plan rejects the idea of tracking past expenses. Instead, you automate your money the day you get paid. You route 50-60% to fixed costs, 10% to investments, 5-10% to savings, and you purposefully designate 20-35% as “Guilt-Free Spending”. Once the bills and savings are automatically funded, you spend that guilt-free money on whatever brings you joy—no tracking required.

4. The Anti-Budget

If looking at spreadsheets makes you want to pull your hair out, use the Anti-Budget (or “Pay Yourself First” method). You set a specific savings/investing goal (say, 20% of your income). On payday, that 20% automatically transfers to your investment accounts. Your fixed bills are on autopay. Whatever is left in your checking account is yours to spend freely. You track absolutely nothing.

The 2025 Budgeting Tech Stack

Forget the paper ledgers. The software you choose can make or break your budgeting habit. I’ve tested the major players, and here is how they stack up.

YNAB (You Need A Budget) YNAB is the undisputed king of Zero-Based Budgeting. It forces you to only budget the cash you currently have on hand. Its credit card handling is brilliant but takes a minute to learn: when you buy $50 of groceries on a credit card, YNAB automatically moves $50 from your grocery budget into a “Credit Card Payment” pile. It’s phenomenal for breaking the paycheck-to-paycheck cycle, but you have to check it daily or weekly.

Monarch Money Monarch has become my go-to recommendation for most people. It’s less opinionated than YNAB and acts more like a holistic dashboard for your entire net worth. The killer feature here is the custom rules engine. You can tell Monarch, “If a charge is from Shell and over $30, categorize it as Gas and tag it as ‘Roadtrip’.”. It practically runs itself once you set it up. It also offers exceptional collaboration tools for couples.

Copilot Money If you are strictly in the Apple ecosystem (Mac and iOS), Copilot is beautifully designed. It uses AI to learn your categorization habits quickly and turns your daily transaction review into a clean, gamified “Inbox” experience. It doesn’t sell your data for ads, which is a massive privacy win.

Google Sheets (The DIY Route) If you refuse to pay a subscription fee, Google Sheets is still incredibly powerful. You can use free add-ons or secure APIs to automatically import your bank transactions into a raw data tab. From there, writing a simple =QUERY function lets you build dynamic, custom dashboards tailored exactly to your brain.

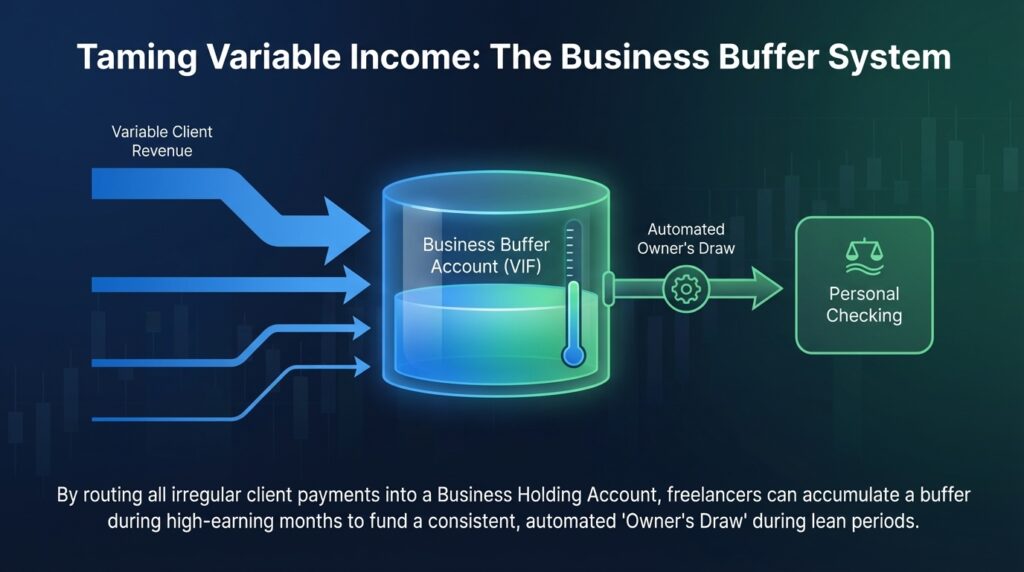

Taming Variable Income and Sinking Funds

If you’re a freelancer or work on commission, generic advice breaks down. When your income fluctuates wildly, you can’t rely on a static monthly template.

The biggest mistake I see freelancers make is forecasting—spending cash today based on an invoice they hope clears tomorrow. The fix is the Variable Income Routing System:

Calculate your minimum baseline expenses.

Send all your freelance revenue to a dedicated Business Checking account.

Set up an automatic weekly or monthly transfer from that business account to your personal account for a fixed “salary”.

During great months, the extra cash stays in the business account, building a buffer. During slow months, you draw from that buffer so your personal “salary” never dips.

You also need Sinking Funds. These are mini-savings accounts for predictable but non-monthly expenses. Instead of being blindsided by a $600 car insurance bill every six months, you divide it by six and put $100 a month into an “Auto Maintenance” sinking fund. Treat it like a monthly bill, and emergencies suddenly become minor inconveniences.

Merging Finances as a Couple

Money fights are a top cause of relationship stress. When you move in together or get married, you generally have three options for your financial architecture :

Fully Merged: All money goes into one giant pot. Great for teamwork, but can lead to resentment if one person feels judged for buying a video game or expensive shoes.

Proportional Split: You keep separate accounts and contribute to shared bills based on income percentages. Fair, but can feel like you’re living with a roommate instead of a spouse.

Yours, Mine, Ours (The Sweet Spot): All income goes into a primary Joint Account to cover housing, utilities, and shared goals. Then, the system automatically transfers an “allowance” into each partner’s private Individual Account. You can spend your individual money on absolutely anything, guilt-free, with zero oversight from your partner.

High-Impact Budgeting Hacks

To close this out, let’s look at a few practical ways to actually create breathing room in your budget:

Audit the Subscriptions: Go through your credit card statements and cancel the streaming services you haven’t watched in a month. Rotate them—pay for Netflix in January, cancel it, and get Hulu in February.

The YouTube DIY Tax: Before calling a professional for a leaky sink or a weird appliance noise, search YouTube. I have saved thousands of dollars doing minor home and auto repairs myself just by following 10-minute tutorials.

Get One Month Ahead: The ultimate goal is to break the paycheck-to-paycheck cycle by using the money you made last month to pay for this month’s expenses. When you reach this point, you no longer care about timing your bills to your paydays. The cash is already sitting there on the 1st of the month.

Creating a budget isn’t about restricting yourself from having fun. It’s about designing an automated system that handles your obligations silently in the background, freeing you up to spend your money—and your mental energy—on the things that actually matter to you.